What slippage in trading is

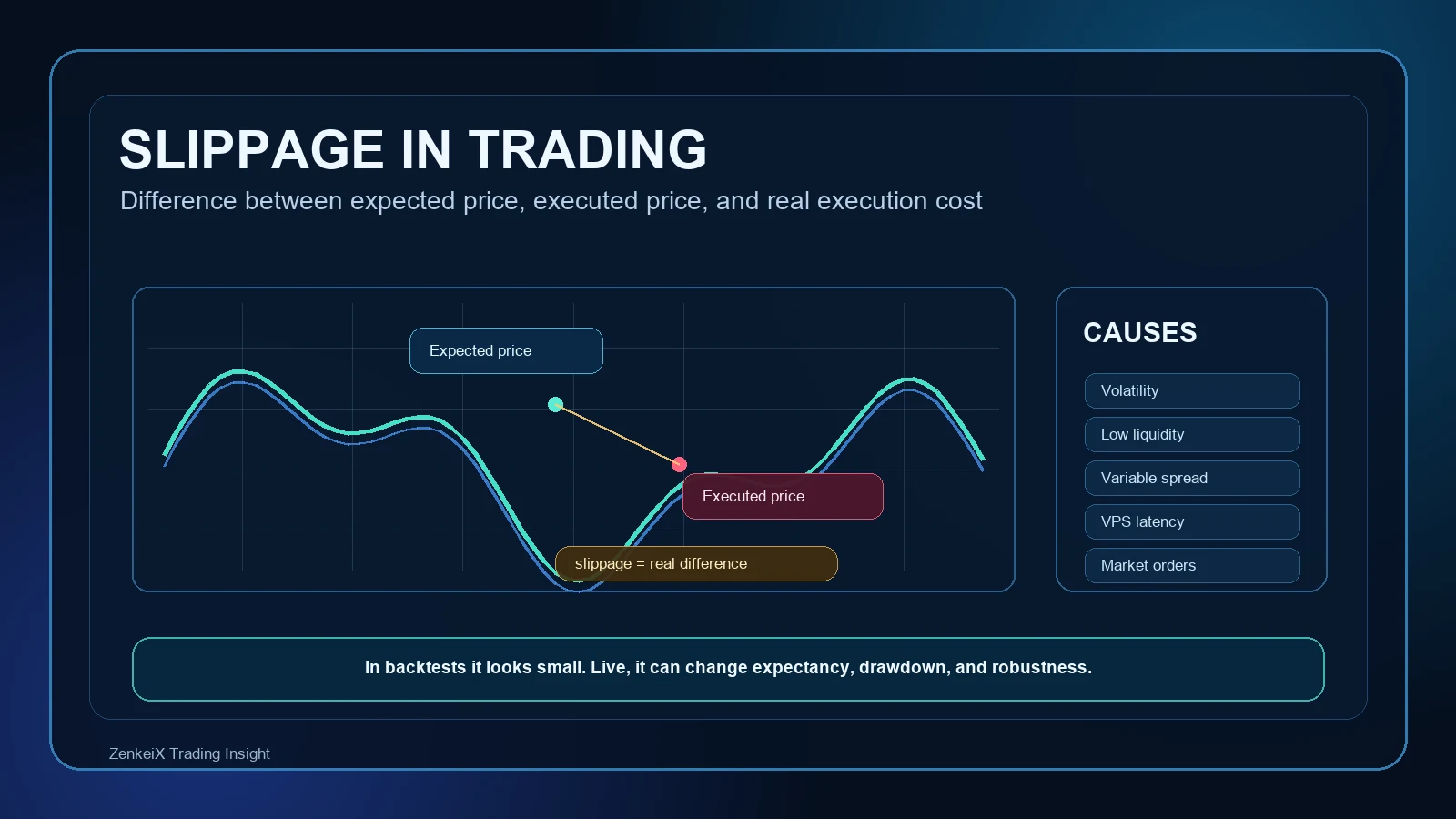

Slippage in trading is the difference between the price you expect when sending an order and the price at which the order is actually executed. It may look like a technical detail, but in an automated system it becomes a performance variable.

If you want to buy at 1.1000 and the order is filled at 1.1003, those 3 points are negative slippage. If execution happens at a better price, slippage is positive. The goal is not to pretend slippage can disappear. The goal is to measure it, model it, and reduce it when it changes the strategy behavior.

The main causes of slippage

Slippage appears when the market moves between order submission and execution. The faster, thinner, or more unstable the market is, the more execution can drift away from the theoretical price.

- Volatility: during news, market opens, or sudden spikes, price can jump through intermediate levels.

- Low liquidity: if there is not enough volume at the desired price, the order is filled at worse levels.

- Variable spread: a widening spread immediately changes the real cost of the trade.

- Latency: VPS, broker, bridge, and server delays can matter.

- Order type: market orders prioritize execution, not price.

This is why slippage should be read with Value at Risk, maximum drawdown, and Profit Factor vs Recovery Factor. It is not just an entry cost. It is a variable that changes risk, return, and robustness.

Why slippage really changes a backtest

A backtest can look perfect because it assumes perfect execution. But a real strategy does not live inside a spreadsheet. It lives inside spread, latency, volatility, liquidity, and broker conditions.

Slippage matters most for systems with tight targets, scalping logic, high trade frequency, or precise risk reward assumptions. If the average take profit is small, a few points of slippage can consume a meaningful part of the edge.

The issue becomes more serious when slippage is not evenly distributed. It often gets worse during the worst moments: news, spikes, gaps, stop loss execution, and sudden volatility. That means it can increase equity curve discomfort exactly when the system is already stressed.

Slippage and Expert Advisors

In Expert Advisors, slippage should not be treated as a secondary detail. An EA can be logically correct and still perform poorly if its execution logic ignores real conditions.

When reviewing an EA, check at least three things: maximum allowed spread, real average slippage, and the difference between backtest and live account. If the system works only with ideal spread and zero slippage, it is probably not robust. It is an optimized report.

This is where Monte Carlo simulation, K-Ratio, and Recovery Factor become useful. A sustainable strategy must survive not only entry logic, but also the real cost of execution.

How to reduce slippage in trading

You cannot control every market tick, but you can design the system so it suffers less slippage and does not depend on unrealistic execution.

- use a VPS close to the broker server when the strategy is latency sensitive;

- avoid automated entries during high impact news if the system is not built for that context;

- filter abnormal spread before sending orders;

- consider limit orders when price matters more than execution probability;

- test the backtest with conservative slippage, not ideal conditions;

- compare demo, live, and MyFxBook reports to measure real execution drift.

Want to know whether your Expert Advisor can handle real execution, spread, and slippage?

We can analyze backtests, operating logs, broker conditions, drawdown, and robustness metrics to understand whether the system is ready to work outside the lab.

FAQ

What is slippage in trading?

It is the difference between expected price and actual execution price. It can be positive or negative, but it should always be considered when evaluating real strategies.

Why does slippage damage a backtest?

Because a backtest without slippage assumes executions that are too clean. In live markets, spread, volatility, latency, and liquidity can worsen entries and exits.

How do you reduce slippage in an Expert Advisor?

With suitable broker and VPS choices, spread filters, trading session rules, market order management, and realistic execution cost testing.

Is slippage always negative?

No. It can also improve execution price, but automated systems should model it prudently because negative slippage tends to appear during the most delicate conditions.